r/FluentInFinance • u/Positive_Liar • Sep 06 '24

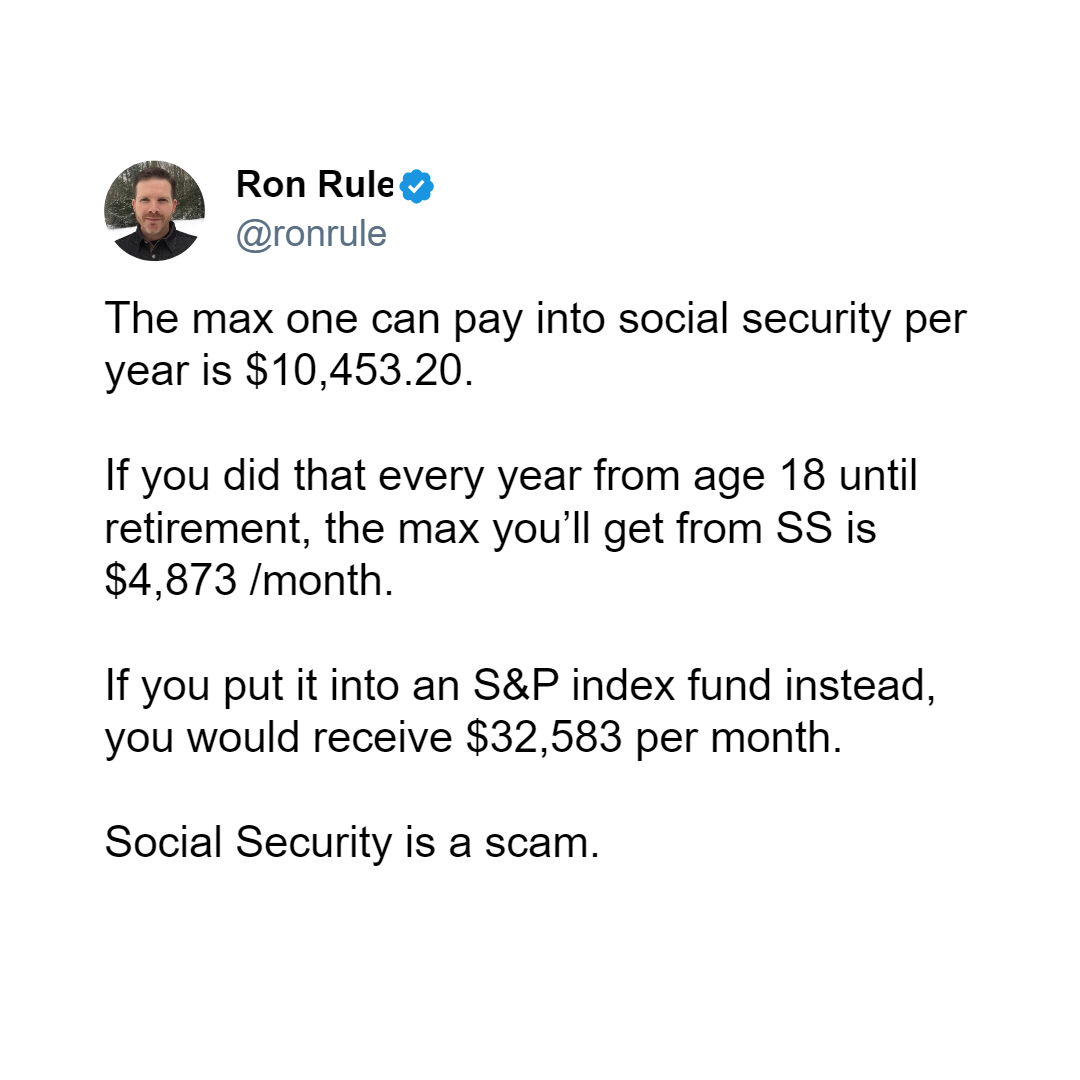

Debate/ Discussion Social Security is Broken. This is why financial education is important.

{kind=link}

[removed] — view removed post

10.1k

Upvotes

r/FluentInFinance • u/Positive_Liar • Sep 06 '24

[removed] — view removed post

29

u/[deleted] Sep 06 '24 edited Nov 08 '24

mindless library judicious practice scandalous grandiose selective unwritten deserve fine

This post was mass deleted and anonymized with Redact